BY Richard Summerfield

US drug distributor Cardinal Health Inc has agreed to acquire Medtronic PLC’s patient monitoring and recovery unit for $6.1bn in cash. However, reaction to the acquisition has been far from positive, with Cardinal’s share price plummeting in the aftermath of the deal announcement.

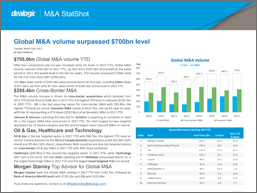

According to a statement announcing the deal, Cardinal will fund the acquisition with $4.5bn of new debt and existing cash. The deal structure has proved unpopular, however. Indeed, Fitch Ratings has raised concerns over Cardinal’s debt and, as a result, lowered its outlook on the healthcare services company. In total, Cardinal’s share price fell 13 percent to $71.40.

On the Medtronic side of the transaction, the company is making moves to shed a number of assets in light of its $50bn acquisition of Irish healthcare product manufacturer Covidien in 2015, in a so-called ‘inversion’ deal.

Cardinal will acquire Medtronic’s patient care, deep vein thrombosis and nutritional insufficiency units which will include 23 product categories in total, encompassing multiple market settings, including brands such as Curity, Kendall, Dover, Argyle and Kangaroo.

“Given the current trends in healthcare, including aging demographics and a focus on post-acute care, this industry-leading portfolio will help us further expand our scope in the operating room, in long-term care facilities and in home healthcare, reaching customers across the entire continuum of care,” said Cardinal's chief executive, George S. Barrett, in a statement.

"This is a positive transaction for all involved - Medtronic, Cardinal Health, and our respective shareholders and employees - who we believe will all thrive under this change in ownership. In addition, it signifies our commitment to disciplined portfolio management," said Omar Ishrak, Medtronic's chairman and chief executive officer.

He continued: "Medtronic has had a specific focus over the past several years on ensuring that we are delivering compelling clinical and economic value to health systems and patients around the world. Ultimately, we came to the conclusion that these products - while truly meaningful to patients in need - are best suited under ownership that can provide the investment and focus that these businesses require. At the same time, we can put these proceeds to work, investing over the long-term in higher returning internal and external opportunities that are more directly aligned with our growth strategies of therapy innovation, globalisation, and economic value."

The deal is expected to close in the second quarter of Medtronic's fiscal year 2018, subject to receipt of customary regulatory approvals and satisfaction of other customary closing conditions.

News: Cardinal Health's dull forecast drags rivals' shares despite Medtronic buy