BY Richard Summerfield

The global IPO market has belied the uncertainty surrounding the global economy, registering the most impressive Q1 in a decade, according to a new report from EY – 'Global IPO Trends: Q1 2017'.

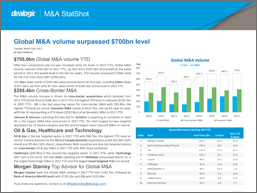

EY’s report reveals that it was the most active first quarter by number of IPOs globally since 2007, with 399 IPOs raising $47.5bn. In terms of year-over-year growth, there was a 92 percent increase in number over 2016, and a 146 percent increase in total value.

The technology sector was the biggest sectoral winner. The industry contributed $6.5bn despite not having the highest number of IPOs. The tech space saw 45 offerings compared to 66 in the industrial sector, which registered proceeds in excess of $4.1bn. By contrast, the telecommunications space was the least active sector, with only six IPOs raising just $351m.

In the US market, 24 IPOs raised $10.8bn, the region’s best performance since Q2 2015, when 72 IPOs raised $14.3bn. The region suffered in comparison to the Asia-Pacific area, which was led by Greater China. In total, Asia-Pacific generated 70 percent of the total number of IPOs, for $16.2bn. However, the US’ performance was still strong. "The first quarter of 2017 was one of the strongest for the US IPO market and established a solid runway for more deals for the remainder of the year”, said Jackie Kelley, EY Americas IPO Markets Leader. “This positive performance should attract more tech and unicorns to the public markets and further open the door for other sectors such as retail, energy, and real estate. With the market currently insulated from the political uncertainty, more companies are expected to enter the filing process."

Dr Martin Steinbach, EY Global and EY EMEIA IPO Leader, said: “This is a promising start to global IPO activity this year. In the face of sustained global economic uncertainty, the first quarter of this year has set the stage for accelerated growth in 2017. Economic fundamentals are improving in the major developed economies. Equity index performance and valuations are trending upward, with several major indices reaching all-time highs. Concurrently, volatility is low, underpinning positive IPO sentiment, which is also supported by the successful US listing of a large technology unicorn."

Report: Global IPO Trends: Q1 2017